At Casca, we envision a future where access to capital is seamless and equitable, particularly for the small businesses that form the backbone of our economy. By harnessing the power of advanced AI and innovative automation, we are redefining the financial landscape to remove barriers and accelerate lending processes for community banks and SBA lenders.

Our platform is designed to transform traditional loan origination with intelligent integration, real-time document analysis, and automation that not only expedites underwriting but also enhances decision quality. Through these innovations, we empower financial institutions to compete on a level playing field with fintech disruptors, unlocking unprecedented value in commercial lending.

Casca is committed to building a future where responsible AI sets new standards for efficiency and fairness, delivering faster, more accurate loan decisions that fuel growth and opportunity for small businesses everywhere. We are not just building technology; we are creating a new paradigm for finance that supports resilient, thriving communities.

Our Review

We've been tracking Casca since they emerged from Y Combinator in 2023, and frankly, we're impressed by how quickly they've gone from Stanford research project to serious fintech contender. Their AI-native approach to loan origination isn't just another "AI washing" story — it's actually solving real problems that have plagued community banks for decades.

What caught our attention first was their bold claim about unlocking $1 trillion in value for banks. That sounds like typical Silicon Valley hyperbole until you dig into what they're actually doing.

The Magic Behind the Machine

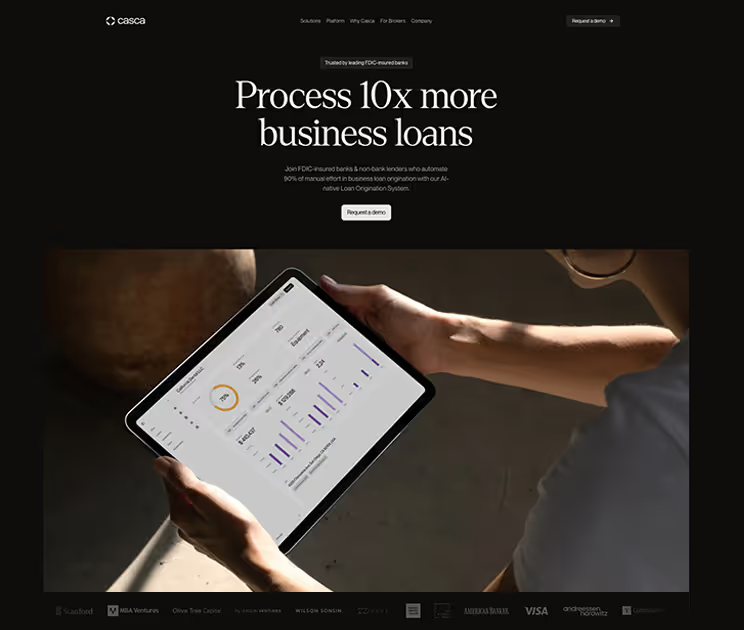

Casca's platform does something we haven't seen done this comprehensively before: it reads and analyzes thousands of pages of loan documents — tax returns, bank statements, financial records — in minutes instead of days. We're talking about AI that can process the kind of paperwork that normally has loan officers pulling all-nighters.

Their 30+ native data integrations mean banks aren't just getting faster processing; they're getting better credit decisions. The platform can pre-qualify borrowers instantly and even handles after-hours applications, which is a game-changer for small business owners who can't always call during banker hours.

Real Results, Not Just Promises

Here's where Casca gets interesting: they're claiming to cut loan cycle times by 5 days and save loan officers 20 hours per week. Those aren't small improvements — that's the difference between a community bank staying competitive or getting steamrolled by fintech lenders.

Their partnership with Live Oak Bank gives us real-world validation. Live Oak isn't some tiny credit union experimenting with new tech; they're a major SBA lender with serious skin in the game. When they integrate Casca's AI into their SBA 7(a) loan process, that tells us the technology actually works.

Why This Matters Now

The timing couldn't be better for Casca. Community banks are getting squeezed from both sides — fintech startups that can approve loans in hours and mega-banks with massive tech budgets. Casca is essentially giving smaller banks superpowers to compete.

That $29 million Series A from Canapi Ventures (who know a thing or two about financial services) suggests we're not the only ones who think they're onto something big. We're curious to see how they handle the inevitable scaling challenges, but their foundation looks solid.

Feature

AI-powered loan origination platform with 30+ native data provider integrations

Automated document collection and rapid analysis of loan-related documents

Instant pre-qualification features for after-hours loan applications

Digital account opening and real-time voice assistant for loan discussions

Online applications with automatic pre-fills and follow-ups to increase lead conversion rates

Jobs

FAQs

Casca